How to Save Money on a Low Income: Practical and Actionable Strategies

Saving money on a low income may seem daunting, but it is absolutely achievable with the right approach. Whether you’re living paycheck to paycheck, managing a family, or working to get out of debt, small, intentional changes can lead to significant savings over time. If you’re searching for effective strategies on how to save money on a low income, this comprehensive guide is here to help.

Thank you for reading this post, don't forget to subscribe!In this post, we’ll focus on realistic, actionable steps that can help you build your financial security, even on a limited income. From creating a budget to exploring new income streams, the strategies here are tailored for individuals and families who need to make the most of what they have.

1. Understanding Your Financial Situation: The Foundation of Saving

The first and most crucial step in saving money on a low income is to fully understand your financial situation. Before making any changes, you need to know where your money is going and how much is coming in. This means a detailed examination of all sources of income and your monthly expenses.

How to Begin:

- Track Your Income: Write down every source of income, including wages, government benefits, side jobs, or child support. This gives you a clear picture of your monthly cash flow.

- Track Your Expenses: Break your expenses into categories:

- Essentials: Rent, groceries, utilities, transportation.

- Non-essentials: Entertainment, dining out, subscriptions.

- Review and Analyze: Once you see how much money you’re spending, it becomes easier to identify areas where you can cut back.

Tip: Use budgeting apps like Mint or PocketGuard to automatically track and categorize your spending. This not only saves time but also helps identify spending patterns that you might not be aware of.

Why This Step Matters:

Understanding your financial situation is empowering. It helps you make informed decisions about where and how to save, and it lays the foundation for better money management habits.

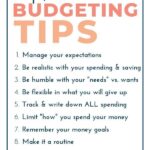

2. Create a Realistic Budget: Your Roadmap to Financial Stability

A budget is a crucial tool for managing your money, especially when funds are limited. It serves as a guide, helping you allocate your income toward essentials first and savings second. Without a budget, it’s easy to lose track of spending and fall short on savings.

Steps to Create a Budget:

- Prioritize Essentials: Start by covering rent/mortgage, utilities, food, transportation, and healthcare costs. These should account for most of your budget.

- Set Limits for Non-Essentials: Allocate a smaller portion of your income for non-essential spending, such as entertainment or eating out.

- Set a Savings Goal: Even if you can only save a small percentage of your income, make it a non-negotiable part of your budget. The earlier you start saving, the more time your money has to grow, even if it’s in small amounts.

Tips for Effective Budgeting:

- Use the 50/30/20 Rule: This popular budgeting framework recommends allocating 50% of your income to necessities, 30% to discretionary spending, and 20% to savings and debt payments. Adjust these percentages based on your personal needs.

- Pay Yourself First: Automate your savings by setting up direct transfers to your savings account each payday. This way, you prioritize savings before discretionary spending.

- Adjust as Needed: A budget should be flexible. If you encounter unexpected expenses, don’t hesitate to adjust your budget accordingly.

Why This Step Matters:

Budgeting helps ensure you don’t spend more than you earn and allows you to set clear financial goals. By knowing exactly where your money goes, you can make conscious choices about spending and saving.

3. Building an Emergency Fund on a Low Income: Start Small but Stay Consistent

An emergency fund is your financial safety net—essential for covering unexpected expenses, such as medical bills, car repairs, or sudden job loss. Even if you’re living on a low income, it’s crucial to start building this fund, no matter how small the initial contributions.

Why You Need an Emergency Fund:

- Protect Against Debt: Without an emergency fund, unexpected expenses often lead to debt or the need for high-interest loans.

- Peace of Mind: Knowing you have a buffer for emergencies reduces financial anxiety.

How to Start Saving:

- Start Small: Aim for an initial goal of $500 to $1,000. Even setting aside $5 or $10 a week can make a difference.

- Automate Your Savings: Set up an automatic transfer from your checking account to your emergency fund after each paycheck.

- Use a High-Yield Savings Account: Consider online banks like Ally Bank or Marcus by Goldman Sachs that offer high-interest rates, helping your savings grow faster without risking it in investments.

Tip: Make saving for emergencies a habit by linking your savings goal to a specific action. For example, every time you skip takeout, transfer that money to your emergency fund.

4. Cutting Unnecessary Expenses: Trim the Fat in Your Budget

To save money on a low income, cutting back on non-essential expenses is one of the fastest ways to free up cash. This doesn’t mean you need to cut out all fun or extras, but identifying areas of waste can help redirect that money toward your savings.

How to Identify Unnecessary Spending:

- Review Subscriptions: Cancel any subscriptions you don’t use regularly. Many people waste money on streaming services, gyms, or apps they rarely use.

- Cut Utility Costs: Simple changes can save money on utilities. Turn off lights, unplug devices, switch to energy-efficient lightbulbs, and lower your thermostat to reduce heating and cooling costs.

- Shop Smarter: Use grocery apps like Ibotta or Fetch Rewards to earn cashback on everyday purchases. Buy generic brands and plan meals ahead to avoid last-minute takeout.

Why Cutting Back Works:

Cutting unnecessary expenses frees up more of your income for essential purchases and savings. Over time, even small adjustments, like brewing your coffee at home or carpooling, can make a big difference in your budget.

Tip: Try a “no-spend” challenge for one week or one month, where you only spend money on essential items. This can help reset your spending habits and highlight how much you can save by cutting out non-essential purchases.

5. Frugal Living Tips to Stretch Your Dollar

Living frugally is about making mindful decisions that help you stretch your income without sacrificing your quality of life. Embracing frugality doesn’t mean giving up everything you enjoy, but it does mean finding cheaper alternatives.

Smart Frugal Living Habits:

- Buy Secondhand: Thrift stores and online marketplaces like Facebook Marketplace or Poshmark offer excellent deals on clothes, furniture, and electronics.

- DIY Where Possible: Learn to fix things around the house or cook more meals at home. YouTube tutorials are free resources for learning DIY skills that can save money on repairs and maintenance.

- Use Public Resources: Libraries, community centers, and public parks offer free entertainment, resources, and programs that can replace paid activities.

- Cashback Apps: Use apps like Rakuten or Dosh to get cash back on everyday purchases like groceries or online shopping.

Why Frugal Living Works:

Frugal living maximizes your income by ensuring that every dollar is spent wisely. You can still enjoy a fulfilling life by finding low-cost or free alternatives for things like entertainment, clothing, and home maintenance.

6. Generating Additional Income: Boost Your Earnings to Save More

Sometimes, cutting costs isn’t enough, and finding ways to increase your income can be a powerful way to save more. Whether it’s taking on a side hustle or selling unused items, every little bit of extra cash helps.

Ideas to Increase Your Income:

- Freelancing: Offer your skills—such as graphic design, writing, or tutoring—on platforms like Upwork, Fiverr, or Freelancer.

- Gig Economy Jobs: Work part-time with companies like Uber, DoorDash, or Instacart to earn extra income during your free time.

- Sell Unused Items: Clean out your closet or garage and sell items you no longer need on platforms like eBay, Poshmark, or Craigslist.

Tip: Any additional income earned from side gigs or freelance work should go directly to savings or paying off debt. Avoid the temptation to increase your spending with new earnings.

7. Take Advantage of Community Assistance Programs

If you’re living on a low income, don’t hesitate to explore community assistance programs available in your area. Many local, state, and federal programs are designed to help individuals and families struggling to make ends meet.

Examples of Assistance Programs:

- SNAP (Supplemental Nutrition Assistance Program): Provides financial assistance for groceries.

- LIHEAP (Low Income Home Energy Assistance Program): Helps cover heating and cooling costs for low-income households.

- Housing Vouchers: Available through HUD, these can help subsidize rent.

- Free or Reduced Price Health Clinics: Offer medical services at little to no cost.

Why This Matters: These programs are designed to alleviate financial pressure on essential expenses, allowing you to redirect more of your income toward savings. Explore local community centers and government websites to see what’s available in your area.

8. Be Strategic About Debt Repayment

Debt can make it incredibly difficult to save money, especially on a low income. However, adopting a strategic debt repayment plan can free up more of your income and reduce the financial burden over time.

Debt Repayment Strategies:

- Snowball Method: Focus on paying off your smallest debts first to build momentum.

- Avalanche Method: Prioritize paying off high-interest debt to save money on interest charges.

- Debt Consolidation: If you have multiple debts, consider consolidating them into one lower-interest payment.

- Negotiate with Creditors: Some creditors may be willing to lower your interest rates or offer payment plans to make your debt more manageable.

Why This Matters: Reducing debt not only frees up more of your monthly income for savings but also reduces the stress of having to manage multiple financial obligations.

9. Meal Planning and Smart Grocery Shopping

Food is one of the largest recurring expenses for most households, but there are ways to reduce your grocery bills without sacrificing quality. Meal planning and smart shopping can significantly cut your costs while ensuring you still eat healthily.

Money-Saving Tips for Groceries:

- Meal Planning: Plan your meals for the week in advance to avoid impulse purchases and wasted food.

- Buy in Bulk: Non-perishable items like rice, beans, and pasta are often cheaper when bought in bulk.

- Use Coupons and Cashback Apps: Take advantage of apps like Ibotta, Fetch, and Coupons.com for discounts and cashback rewards.

- Shop Sales and Discounts: Check your grocery store’s circulars for sales and stock up on items you frequently use when they’re on discount.

Why This Matters: Reducing your grocery bill can free up hundreds of dollars per year that can be redirected toward savings or other important expenses.

10. Set Short-Term and Long-Term Financial Goals

While living on a low income can make it feel like saving for the future is impossible, setting both short-term and long-term financial goals can help you stay motivated and focused.

How to Set Financial Goals:

- Short-Term Goals: These could be saving a specific amount for an emergency fund or paying off a small debt. These goals are achievable within 6 months to a year.

- Long-Term Goals: Think about larger goals like saving for retirement, buying a home, or building a more substantial emergency fund. These goals might take 5-10 years or longer.

- Break Down Your Goals: Break large goals into smaller, actionable steps to keep your progress measurable and attainable.

Why This Matters: Having clear financial goals gives you direction and purpose, helping you prioritize your spending and savings habits.

Conclusion: Financial Stability is Within Reach

Saving money on a low income is entirely possible, and with careful planning, small changes, and disciplined spending, you can build long-term financial security. By understanding your finances, budgeting, cutting unnecessary expenses, and maximizing both free resources and extra income, you’ll make steady progress toward your financial goals.

Key Takeaways:

- Understand Your Finances: Track your income and expenses carefully.

- Budget Wisely: Allocate your money toward essential expenses first, then savings.

- Cut Costs: Identify unnecessary spending and reduce your daily costs.

- Build an Emergency Fund: Start small but be consistent in saving for unexpected expenses.

- Increase Your Income: Explore side hustles or freelance opportunities to boost your earnings.

For more detailed strategies on how to improve your savings, check out our Long Term Investment Strategies for tips on how to grow your savings over time. Additionally, explore this Comprehensive Budgeting Guide for expert advice on managing your finances.

By following these steps, you’ll be well on your way to saving money, achieving your financial goals, and gaining peace of mind, even on a limited income.

Frequently Asked Questions

1. How can I save money on a low income if I’m living paycheck to paycheck?

Saving money on a low income is possible, even if you’re living paycheck to paycheck. Start by tracking all your expenses and creating a budget that prioritizes essentials. Cut back on non-essential spending and set up small, automatic transfers into a savings account, even if it’s just $5 or $10 per week. Every little bit helps when trying to save money on a low income.

2. What’s the best way to budget to save money on a low income?

To save money on a low income, use a simple budgeting method like the 50/30/20 rule: 50% of your income goes to essentials, 30% to discretionary spending, and 20% to savings. Adjust these percentages based on your income and focus on reducing discretionary expenses. Stick to your budget by tracking all spending and reallocating any extra money toward savings.

3. Can I save money on a low income if I have debt?

Yes, you can save money on a low income even if you have debt. Prioritize paying off high-interest debt using methods like the avalanche or snowball method, and dedicate any additional funds to savings. Even setting aside a small amount while paying off debt can help build an emergency fund, preventing future debt when unexpected expenses arise.

4. How do I save money on a low income with high utility bills?

To save money on a low income with high utility bills, reduce your energy consumption by turning off lights, unplugging electronics, using energy-efficient appliances, and lowering your thermostat. You can also contact your utility provider to explore budget billing or low-income assistance programs that could reduce your monthly bills.

5. Is it possible to build an emergency fund and save money on a low income?

Absolutely! Building an emergency fund while trying to save money on a low income is possible by starting small. Set aside as little as $10 a week in a separate savings account. Over time, this will accumulate into a cushion for unexpected expenses. Automating your savings transfers can also help you consistently grow your emergency fund.

6. What are some ways to cut food costs and save money on a low income?

To save money on a low income, plan your meals ahead of time, use grocery store discounts, buy generic brands, and cook at home instead of eating out. Consider using cashback apps or coupons to further reduce costs. Bulk buying and freezing can also help you save money over time by reducing the frequency of grocery trips.

7. Can I save money on a low income while raising children?

Yes, you can save money on a low income while raising children by using budget-friendly strategies such as buying secondhand clothes, toys, and equipment, meal planning to reduce food costs, and utilizing community programs for free or low-cost childcare, activities, and school supplies. Prioritize saving for future family needs, even if it’s just a small amount each month.

8. What is the most important tip to save money on a low income?

The most important tip to save money on a low income is to create a realistic budget that tracks every dollar. Prioritize essential expenses, eliminate unnecessary spending, and automate savings, even if it’s just a small amount. Consistency and discipline with your budget are key to successfully saving money over time.

9. How can I save money on a low income without giving up all entertainment?

You can save money on a low income without giving up entertainment by seeking free or low-cost alternatives. Look for free community events, use the library for books and movies, or explore streaming services with affordable plans. Many entertainment options don’t have to be expensive—you just need to find budget-friendly alternatives.

10. Are there any assistance programs that help people save money on a low income?

Yes, many local, state, and federal assistance programs are designed to help individuals save money on a low income. Programs like SNAP for groceries, LIHEAP for energy bills, and housing assistance programs can free up money for savings by reducing essential expenses. Look into what’s available in your community to maximize savings potential.

Comments are closed.