Introduction to Financial Planning

Financial planning is the foundation upon which secure financial futures are built. It is an ongoing process that helps individuals and families achieve their financial goals through prudent management of their resources. Unlike merely saving money or budgeting, financial planning is a comprehensive approach that covers everything from budgeting and investing to retirement and estate planning. Understanding its significance and how to implement effective strategies can mean the difference between financial stability and financial hardship.

What is Financial Planning?

At its core, financial planning is the process of creating a roadmap to achieve your financial goals. It involves assessing your current financial situation, setting realistic goals, and developing strategies to achieve those goals while managing risks. The essence of financial planning is not just about accumulating wealth but also about protecting it, ensuring that you can meet both your current and future financial needs.

A good financial plan takes into account various aspects such as income, expenses, investments, insurance, taxes, and retirement. It helps you make informed decisions about how to allocate your resources effectively, ensuring that you can live comfortably while preparing for the future.

Importance of Financial Planning

The importance of financial planning cannot be overstated. A well-thought-out financial plan provides clarity and direction, enabling you to make informed financial decisions with confidence. It helps in identifying and mitigating financial risks, ensuring that you are prepared for life’s unexpected events. Furthermore, financial planning allows you to take advantage of opportunities for growth, such as investing in stocks or starting a business, while managing the risks associated with these activities.

Financial planning is essential for everyone, regardless of income level. Whether you’re just starting out in your career, raising a family, or approaching retirement, a financial plan can help you achieve your goals and secure your financial future. Without a plan, it’s easy to get off track, overspend, or miss opportunities to grow your wealth.

The Basics of Budgeting

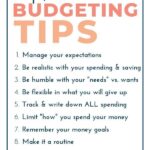

Budgeting is the cornerstone of any financial plan. It is the process of creating a plan to spend your money wisely. By budgeting, you ensure that you have enough money for the things you need and want, while also setting aside funds for savings and investments.

Creating a Monthly Budget

The first step in budgeting is to create a monthly budget. Start by listing all of your sources of income, including your salary, bonuses, and any other income streams. Next, list all of your expenses, including fixed expenses like rent or mortgage payments, utilities, and insurance, as well as variable expenses like groceries, entertainment, and travel.

Once you have a clear picture of your income and expenses, you can start to allocate your money accordingly. Make sure to prioritize essential expenses, such as housing, utilities, and food, before allocating funds for discretionary spending. It’s also important to include savings and investments in your budget. Aim to save at least 20% of your income each month, if possible.

Tracking Expenses

Tracking your expenses is crucial to sticking to your budget. Without tracking, it’s easy to overspend or lose sight of where your money is going. There are various tools and apps available that can help you track your spending automatically. Alternatively, you can track your expenses manually using a spreadsheet or a notebook.

Tracking your expenses regularly allows you to identify areas where you may be overspending and make adjustments as needed. It also helps you stay on track with your financial goals, ensuring that you’re not only covering your expenses but also saving and investing for the future.

Identifying Needs vs. Wants

One of the biggest challenges in budgeting is distinguishing between needs and wants. Needs are the essential expenses that you must pay to live, such as housing, utilities, food, and transportation. Wants, on the other hand, are the non-essential expenses that add comfort or pleasure to your life, such as dining out, vacations, or luxury items.

When creating your budget, it’s important to prioritize your needs over your wants. This doesn’t mean you can’t enjoy the things you want, but it does mean being mindful of your spending and ensuring that you’re not sacrificing your financial goals for short-term gratification.

Setting Financial Goals

Setting financial goals is a crucial step in financial planning. Goals give you a target to aim for and help you stay motivated and focused on your financial journey. Whether you’re saving for a down payment on a house, planning for retirement, or building an emergency fund, having clear, measurable goals can make the process more manageable and achievable.

Short-Term Financial Goals

Short-term financial goals are those that you plan to achieve within the next one to three years. These might include saving for a vacation, paying off a credit card, or building an emergency fund. Short-term goals are typically smaller and more immediate, but they are just as important as long-term goals.

Setting short-term financial goals helps you build momentum and create good financial habits. By achieving these smaller goals, you gain confidence and motivation to tackle larger, long-term goals.

Long-Term Financial Goals

Long-term financial goals are those that you plan to achieve in five years or more. These might include buying a home, funding your children’s education, or saving for retirement. Long-term goals typically require more planning and discipline, as they often involve larger amounts of money and longer time frames.

When setting long-term financial goals, it’s important to break them down into smaller, manageable steps. For example, if you’re saving for retirement, you might set a goal to contribute a certain amount to your retirement account each year. By breaking down your long-term goals, you make them more achievable and less overwhelming.

SMART Goals in Financial Planning

One effective way to set financial goals is to use the SMART criteria. SMART stands for Specific, Measurable, Achievable, Relevant, and Time-bound. By applying these criteria to your financial goals, you can ensure that they are clear, realistic, and attainable.

- Specific: Your goal should be clear and specific. For example, instead of saying, “I want to save money,” say, “I want to save $5,000 for a down payment on a house.”

- Measurable: You should be able to track your progress toward your goal. For example, “I will save $500 per month until I reach my $5,000 goal.”

- Achievable: Your goal should be realistic and within your reach. Consider your income, expenses, and other financial obligations when setting your goal.

- Relevant: Your goal should align with your overall financial objectives. For example, saving for a down payment on a house might be relevant if homeownership is important to you.

- Time-bound: Your goal should have a deadline. For example, “I want to save $5,000 in the next 10 months.”

Building an Emergency Fund

An emergency fund is a crucial component of any financial plan. It provides a financial safety net in case of unexpected expenses or financial emergencies, such as medical bills, car repairs, or job loss. Without an emergency fund, you may be forced to rely on credit cards or loans, which can lead to debt and financial stress.

Importance of an Emergency Fund

An emergency fund gives you peace of mind knowing that you have money set aside for unexpected expenses. It allows you to handle financial emergencies without derailing your long-term financial goals or going into debt. An emergency fund also provides financial stability, ensuring that you’re not living paycheck to paycheck.

How Much to Save in an Emergency Fund

The amount you should save in your emergency fund depends on your individual circumstances, such as your income, expenses, and financial obligations. A common rule of thumb is to save at least three to six months’ worth of living expenses. However, if you have a high level of job security or additional sources of income, you may be able to save less.

On the other hand, if you have a family, high fixed expenses, or an unstable income, you may want to save more. The goal is to have enough money in your emergency fund to cover your essential expenses for a few months in case of a financial emergency.

Where to Keep Your Emergency Fund

Your emergency fund should be easily accessible, but not so accessible that you’re tempted to dip into it for non-emergencies. A high-yield savings account is a good option for your emergency fund, as it offers easy access to your money while earning some interest.

Avoid keeping your emergency fund in investments like stocks or mutual funds, as these can fluctuate in value and may not be readily available when you need them. The key is to keep your emergency fund in a safe, liquid account where you can access it quickly in case of an emergency.

Debt Management Strategies

Debt can be a major obstacle to achieving your financial goals, but with careful planning and discipline, it is possible to manage and eliminate debt over time. Understanding the difference between good debt and bad debt, as well as implementing effective repayment strategies, can help you take control of your finances and work toward a debt-free future.

Understanding Good Debt vs. Bad Debt

Not all debt is created equal. Good debt is typically used to purchase assets that appreciate in value or generate income, such as a mortgage on a home or a student loan for education. These types of debt can be considered investments in your future, as they have the potential to increase your net worth over time.

Bad debt, on the other hand, is typically used to purchase items that depreciate in value or have no long-term financial benefit, such as credit card debt or car loans. Bad debt can be a drain on your finances, as it often comes with high interest rates and can take years to pay off.

Debt Repayment Methods (Avalanche vs. Snowball)

There are two popular methods for paying off debt: the avalanche method and the snowball method. The avalanche method involves paying off your debts with the highest interest rates first, while the snowball method involves paying off your smallest debts first.

- Avalanche Method: This method can save you the most money in interest over time, as you prioritize paying off high-interest debt first. Once your highest-interest debt is paid off, you move on to the next highest, and so on. The avalanche method is the most cost-effective way to pay off debt, but it requires discipline and patience.

- Snowball Method: This method focuses on paying off your smallest debts first, regardless of interest rate. The idea is that by quickly eliminating smaller debts, you build momentum and motivation to tackle larger debts. The snowball method can be more psychologically rewarding, but it may cost you more in interest over time.

Tips for Staying Out of Debt

Staying out of debt requires careful planning and discipline. Here are some tips to help you avoid falling into the debt trap:

- Live Within Your Means: Avoid spending more than you earn. Stick to a budget and prioritize saving and investing over unnecessary spending.

- Avoid High-Interest Debt: Be cautious with credit cards and other forms of high-interest debt. If you do use credit, make sure to pay off your balance in full each month.

- Build an Emergency Fund: An emergency fund can help you avoid relying on credit cards or loans in case of unexpected expenses.

- Pay Off Debt Quickly: If you do have debt, focus on paying it off as quickly as possible to minimize interest charges and free up your income for other financial goals.

- Seek Help if Needed: If you’re struggling with debt, consider seeking help from a financial advisor or credit counseling service. They can help you develop a plan to manage and pay off your debt.

Investment Planning

Investing is a key component of financial planning. It involves putting your money to work to grow your wealth over time. By investing in a diversified portfolio of assets, you can increase your chances of achieving your financial goals, whether it’s saving for retirement, buying a home, or funding your child’s education.

Basics of Investing

Investing involves buying assets that have the potential to increase in value over time. The most common types of investments include stocks, bonds, and mutual funds. Each type of investment carries a different level of risk and potential return, so it’s important to understand the basics before you start investing.

Types of Investments (Stocks, Bonds, Mutual Funds, ETFs)

- Stocks: When you buy a stock, you’re buying a share of ownership in a company. Stocks have the potential for high returns, but they also come with a higher level of risk.

- Bonds: Bonds are loans that you make to a company or government in exchange for interest payments. Bonds are generally considered safer than stocks, but they also offer lower returns.

- Mutual Funds: Mutual funds pool money from many investors to buy a diversified portfolio of stocks, bonds, or other securities. Mutual funds offer diversification and professional management, but they also come with fees.

- ETFs (Exchange-Traded Funds): ETFs are similar to mutual funds but trade on stock exchanges like individual stocks. ETFs offer diversification and lower fees, making them a popular choice for investors.

Risk Tolerance and Asset Allocation

Your risk tolerance is your ability and willingness to take on risk in your investments. It depends on factors such as your age, financial goals, and investment experience. Generally, the younger you are, the more risk you can afford to take, as you have more time to recover from potential losses.

Asset allocation is the process of dividing your investment portfolio among different asset classes, such as stocks, bonds, and cash, to balance risk and return. A well-diversified portfolio can help you achieve your financial goals while managing risk.

Importance of Diversification in Investments

Diversification is the practice of spreading your investments across different asset classes, industries, and geographic regions to reduce risk. By diversifying your portfolio, you can protect yourself against significant losses if one investment or sector underperforms.

For example, if you only invest in stocks and the stock market crashes, your entire portfolio could take a hit. However, if you diversify by investing in bonds, real estate, and international stocks, you can reduce your overall risk and increase your chances of achieving positive returns.

Retirement Planning

Retirement planning is a critical aspect of financial planning, as it ensures that you have enough money to support yourself in your later years. Whether you’re just starting your career or nearing retirement age, it’s never too early (or too late) to start planning for retirement.

Why Start Early on Retirement Planning

The earlier you start saving for retirement, the more time your money has to grow. Thanks to the power of compound interest, even small contributions can grow significantly over time. Starting early also allows you to take more risks in your investments, which can lead to higher returns.

If you wait too long to start saving for retirement, you may need to save a larger percentage of your income or delay your retirement to achieve your goals. By starting early, you give yourself more options and flexibility in retirement.

Types of Retirement Accounts (401(k), IRA, Roth IRA)

There are several types of retirement accounts that you can use to save for retirement, each with its own set of benefits and limitations:

- 401(k): A 401(k) is an employer-sponsored retirement plan that allows you to contribute a portion of your salary to a tax-deferred investment account. Many employers offer matching contributions, which can significantly boost your retirement savings.

- IRA (Individual Retirement Account): An IRA is a tax-advantaged retirement account that you can open on your own. Contributions to a traditional IRA are tax-deductible, and your investments grow tax-deferred until you withdraw them in retirement.

- Roth IRA: A Roth IRA is similar to a traditional IRA, but contributions are made with after-tax dollars. This means that your withdrawals in retirement are tax-free, making a Roth IRA a good option for those who expect to be in a higher tax bracket in retirement.

Calculating How Much You Need for Retirement

Determining how much you need to save for retirement depends on factors such as your desired retirement lifestyle, expected expenses, and life expectancy. A common rule of thumb is to aim to replace 70% to 80% of your pre-retirement income in retirement.

To calculate how much you need to save, start by estimating your annual expenses in retirement. Then, subtract any expected income from Social Security, pensions, or other sources. The difference is the amount you’ll need to cover with your retirement savings.

Insurance and Risk Management

Insurance is a key component of financial planning, as it helps protect your assets and provides financial security in case of unexpected events. Understanding the different types of insurance and how much coverage you need is essential to managing risk in your financial plan.

Role of Insurance in Financial Planning

Insurance helps protect you and your family from financial loss due to unforeseen events, such as illness, disability, or death. It provides a safety net, ensuring that you’re not left financially devastated in the event of an emergency.

Without adequate insurance coverage, you may be forced to dip into your savings or go into debt to cover unexpected expenses. By including insurance in your financial plan, you can protect your assets and ensure that your financial goals remain on track.

Types of Insurance (Health, Life, Disability)

- Health Insurance: Health insurance covers medical expenses, including doctor visits, hospital stays, and prescription medications. It is essential for protecting yourself from the high cost of healthcare.

- Life Insurance: Life insurance provides financial support to your beneficiaries in the event of your death. It can be used to cover funeral expenses, pay off debts, or provide income replacement for your family.

- Disability Insurance: Disability insurance provides income replacement if you’re unable to work due to illness or injury. It helps ensure that you can continue to meet your financial obligations even if you’re unable to earn a paycheck.

How Much Insurance Do You Really Need?

The amount of insurance you need depends on your individual circumstances, including your income, expenses, and financial obligations. As a general rule, you should have enough life insurance to cover your debts and provide for your family’s needs in case of your death.

For health and disability insurance, consider your current health status, occupation, and risk factors. If you have dependents, it’s especially important to have adequate coverage to ensure that your family is protected in case of an emergency.

Tax Planning

Tax planning is an essential aspect of financial planning, as it helps you minimize your tax liability and maximize your savings. By understanding how taxes affect your income, investments, and retirement accounts, you can develop strategies to reduce your tax burden and keep more of your hard-earned money.

Understanding Tax Brackets and Deductions

Your tax bracket determines the rate at which your income is taxed. The U.S. tax system is progressive, meaning that higher income levels are taxed at higher rates. Understanding your tax bracket can help you make informed decisions about income, investments, and deductions.

Deductions reduce your taxable income, lowering your overall tax liability. Common deductions include mortgage interest, charitable contributions, and medical expenses. By maximizing your deductions, you can reduce the amount of income that’s subject to taxes.

Tax-Efficient Investment Strategies

There are several tax-efficient strategies you can use to minimize the taxes on your investments:

- Tax-Deferred Accounts: Contributing to tax-deferred accounts, such as a 401(k) or traditional IRA, allows your investments to grow tax-free until you withdraw them in retirement.

- Roth Accounts: Contributions to Roth accounts are made with after-tax dollars, but withdrawals in retirement are tax-free. Roth accounts are a good option if you expect to be in a higher tax bracket in retirement.

- Tax-Loss Harvesting: Tax-loss harvesting involves selling investments that have lost value to offset gains in other investments, reducing your overall tax liability.

Retirement Accounts and Tax Benefits

Retirement accounts offer significant tax benefits that can help you grow your savings more quickly. Contributions to traditional retirement accounts, such as a 401(k) or IRA, are tax-deductible, reducing your taxable income. Additionally, the earnings on your investments grow tax-deferred, allowing you to accumulate wealth more quickly.

Roth retirement accounts offer a different set of tax benefits. While contributions are made with after-tax dollars, withdrawals in retirement are tax-free. This can be especially advantageous if you expect to be in a higher tax bracket in retirement.

Estate Planning

Estate planning is the process of arranging for the management and disposal of your estate after your death. It involves creating legal documents, such as a will or trust, to ensure that your assets are distributed according to your wishes. Estate planning also includes planning for potential inheritance taxes and ensuring that your loved ones are taken care of.

Importance of Estate Planning

Estate planning is important for everyone, regardless of the size of your estate. Without an estate plan, your assets may be distributed according to state law, which may not align with your wishes. An estate plan ensures that your assets are distributed according to your preferences and that your loved ones are provided for.

Essential Estate Planning Documents (Wills, Trusts, Power of Attorney)

- Will: A will is a legal document that outlines how your assets will be distributed after your death. It also allows you to appoint a guardian for your minor children and name an executor to manage your estate.

- Trust: A trust is a legal arrangement that allows you to transfer assets to a trustee to manage on behalf of your beneficiaries. Trusts can be used to minimize estate taxes, avoid probate, and ensure that your assets are managed according to your wishes.

- Power of Attorney: A power of attorney is a legal document that gives someone else the authority to make decisions on your behalf if you’re unable to do so. This can include financial decisions, medical decisions, or both.

Planning for Inheritance Taxes

Inheritance taxes can significantly reduce the value of the assets that you pass on to your heirs. By planning for these taxes, you can minimize their impact and ensure that your loved ones receive the maximum benefit from your estate.

One strategy for minimizing inheritance taxes is to set up a trust, which can help reduce the taxable value of your estate. Additionally, gifting assets to your heirs during your lifetime can reduce the size of your estate and minimize the tax burden on your heirs.

Teaching Financial Literacy to Children

Teaching financial literacy to children is an important part of financial planning, as it helps them develop the skills and knowledge they need to manage their finances as adults. By introducing financial concepts early on, you can set your children up for a lifetime of financial success.

Importance of Teaching Kids About Money

Financial literacy is an essential life skill that can help children make informed decisions about money, avoid debt, and build wealth over time. Teaching kids about money from a young age can also help them develop good financial habits, such as saving, budgeting, and investing.

Age-Appropriate Financial Lessons

- Young Children (Ages 3-7): Introduce basic concepts like saving and spending by giving your child a small allowance and encouraging them to save for a toy or treat.

- Pre-Teens (Ages 8-12): Teach your child about budgeting and the importance of making wise spending choices. You can also introduce the concept of earning money by offering chores or small jobs.

- Teens (Ages 13-18): Teach your teenager about more complex financial concepts, such as credit, debt, and investing. Encourage them to open a savings account and start saving for a car or college.

Tools and Resources for Teaching Financial Literacy to Kids

There are many tools and resources available to help parents teach financial literacy to their children. These include educational games, books, and apps that make learning about money fun and engaging. Additionally, many banks and credit unions offer financial literacy programs for kids and teens.

Financial Planning for Different Stages

Financial planning is not a one-size-fits-all process. Your financial needs and goals will change over time, and it’s important to adjust your financial plan accordingly. Whether you’re in your 20s, 30s, 40s, or beyond, there are key financial milestones and strategies to consider at each stage of life.

Financial Planning in Your 20s, 30s, 40s, 50s, and Beyond

- 20s: In your 20s, focus on building a strong financial foundation by creating a budget, establishing an emergency fund, and starting to save for retirement. Avoid taking on unnecessary debt and focus on building good credit.

- 30s: In your 30s, continue to build your savings and investments while also focusing on major financial goals, such as buying a home or starting a family. Make sure to have adequate insurance coverage and start planning for your children’s education.

- 40s: In your 40s, prioritize paying off debt, such as your mortgage or student loans, and continue to build your retirement savings. Consider working with a financial planner to ensure that you’re on track to meet your long-term goals.

- 50s: In your 50s, focus on maximizing your retirement savings and paying off any remaining debt. Consider adjusting your investment strategy to reduce risk as you approach retirement.

- 60s and Beyond: In your 60s and beyond, focus on preserving your wealth and ensuring that you have enough income to support your retirement lifestyle. Consider your estate planning needs and ensure that your assets are protected.

Adjusting Your Financial Plan as You Age

As you age, your financial priorities will change, and it’s important to adjust your financial plan accordingly. This may involve shifting your investment strategy, adjusting your savings goals, or updating your estate plan.

Regularly reviewing and updating your financial plan ensures that it remains aligned with your current financial situation and goals. Working with a financial planner can help you navigate these changes and make informed decisions about your financial future.

Key Milestones and Financial Goals for Each Decade

- 20s: Build credit, establish an emergency fund, start saving for retirement.

- 30s: Buy a home, start a family, save for your children’s education.

- 40s: Pay off debt, maximize retirement savings, invest for the future.

- 50s: Prepare for retirement, pay off remaining debt, protect your assets.

- 60s and Beyond: Retire comfortably, preserve wealth, ensure a secure estate plan.

Common Financial Planning Mistakes

Even with the best intentions, it’s easy to make mistakes in financial planning. However, by being aware of common pitfalls, you can avoid them and stay on track with your financial goals.

Not Having a Plan

One of the biggest mistakes people make is not having a financial plan at all. Without a plan, it’s easy to lose sight of your financial goals and make impulsive decisions that can derail your progress.

Underestimating Expenses

Another common mistake is underestimating your expenses. This can lead to overspending and difficulty meeting your financial goals. It’s important to create a realistic budget that accounts for all of your expenses, including those that may be irregular or unexpected.

Ignoring Inflation in Planning

Inflation can erode the value of your savings over time, making it harder to achieve your financial goals. It’s important to account for inflation when setting your savings and investment goals, especially for long-term goals like retirement.

Tools and Resources for Financial Planning

There are many tools and resources available to help you create and manage your financial plan. From budgeting apps to investment tracking tools, these resources can help you stay on top of your finances and make informed decisions.

Budgeting Apps and Software

Budgeting apps and software can help you create and stick to a budget. Some popular options include Mint, YNAB (You Need a Budget), and Personal Capital. These tools allow you to track your income and expenses, set financial goals, and monitor your progress.

Investment Tracking Tools

Investment tracking tools can help you monitor your investment portfolio and stay on track with your financial goals. Some popular options include Morningstar, Betterment, and Vanguard. These tools provide insights into your investment performance, asset allocation, and risk tolerance.

Working with a Financial Planner

Working with a financial planner can provide personalized advice and guidance to help you achieve your financial goals. A financial planner can help you create a comprehensive financial plan, manage your investments, and navigate complex financial decisions.

Financial Planning FAQs

How often should I review my financial plan?

It’s a good idea to review your financial plan at least once a year or whenever you experience a major life event, such as getting married, having a child, or changing jobs. Regular reviews ensure that your plan remains aligned with your current financial situation and goals.

What’s the difference between saving and investing?

Saving involves setting aside money for short-term goals or emergencies, while investing involves putting your money to work to grow your wealth over time. Savings are typically kept in low-risk, easily accessible accounts, while investments are made in assets like stocks, bonds, and mutual funds, which have the potential for higher returns.

How much should I save for retirement?

The amount you need to save for retirement depends on factors such as your desired retirement lifestyle, expected expenses, and life expectancy. A common rule of thumb is to aim to replace 70% to 80% of your pre-retirement income in retirement. Working with a financial planner can help you determine how much you need to save based on your specific situation.

What should I prioritize: paying off debt or investing?

Whether you should prioritize paying off debt or investing depends on the interest rates on your debt and your investment returns. If you have high-interest debt, it’s generally a good idea to pay it off first. However, if your investments are likely to generate higher returns than the interest on your debt, you may want to prioritize investing. It’s important to strike a balance between paying off debt and investing to achieve your financial goals.

Do I need a financial planner?

While it’s possible to manage your finances on your own, a financial planner can provide personalized advice and guidance to help you achieve your financial goals. A financial planner can help you create a comprehensive financial plan, manage your investments, and navigate complex financial decisions. If you’re unsure about your financial situation or need help developing a plan, working with a financial planner can be beneficial.

How can I make sure my financial plan is tax-efficient?

To ensure that your financial plan is tax-efficient, consider strategies such as contributing to tax-advantaged retirement accounts, using tax-loss harvesting, and taking advantage of deductions and credits. Working with a tax advisor or financial planner can help you develop a tax-efficient financial plan that minimizes your tax liability while maximizing your savings.

Conclusion

Financial planning is an essential process that helps you achieve your financial goals and secure your future. By creating a comprehensive financial plan that includes budgeting, saving, investing, and risk management, you can build a strong financial foundation and navigate the challenges of life with confidence. Whether you’re just starting out or nearing retirement, it’s never too late to start planning for your financial future. By avoiding common mistakes and taking advantage of the tools and resources available, you can achieve financial success and live the life you’ve always dreamed of.

Selecting a trustworthy financial advisor is a crucial step in financial planning. If you’re looking for guidance on how to choose the right advisor, check out our detailed guide on How to Select a Safe Financial Advisor 2024.

Comments are closed.