Thriving on a Budget: Practical Budgeting Tips & Money-Saving Strategies for Low-Income Earners

Keywords: budgeting tips, saving money, low salary strategies, frugal living

Introduction

Living on a low salary doesn’t mean you can’t build financial stability, reach goals, or enjoy life. With the right budgeting tips and frugal living strategies, many people stretch every dollar further, reduce stress, and create real progress toward savings and freedom. This article gives you a resourceful, empowering plan—practical steps, real examples, and tools you can use today to save money, manage expenses, and thrive even when your income is limited.

Read on to learn how to take control of your money with low salary strategies that are realistic and sustainable. You’ll find a step-by-step budgeting system, everyday ways to cut costs without sacrifice, income-boosting ideas, safety nets to protect your progress, and a quick checklist to get started now.

Why Budgeting Matters on a Low Income

Budgeting is the foundation of financial security—especially on a tight budget. When every dollar counts, a simple plan reduces waste, prevents surprises, and lets you prioritize essentials and goals.

- Clarity: Know where your money goes so you can make intentional choices.

- Control: Avoid overdrafts, late fees, and the stress from unpredictable bills.

- Progress: Even small, consistent savings compound into meaningful emergency funds and future opportunities.

Quick stat: People who actively budget are far more likely to build emergency savings and avoid high-cost credit. Small changes add up faster than you think.

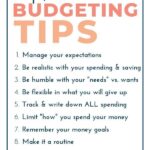

Step-by-Step Budgeting Tips for Low-Income Earners

1. Track every dollar for 30 days

Start with awareness. For one month, record all income and every expense—bills, coffee, transit, tips, cash purchases. Use a notebook, spreadsheet, or an app (Mint, EveryDollar, or a simple Google Sheet).

Outcome: You’ll spot small leaks (subscription services, impulse purchases) that become obvious targets for saving.

2. Build a realistic zero-based budget

A zero-based budget assigns every dollar a job. Income minus expenses equals zero—every dollar is either spent, saved, or allocated to debt repayment.

- List after-tax income for the month.

- Allocate fixed essentials first: rent, utilities, groceries, transportation, minimum debt payments.

- Assign amounts to savings and irregular costs (medical, clothing, car repairs).

- Designate a small “fun” allowance to prevent burnout.

3. Prioritize an emergency fund

Start small: aim for $500–$1,000 as an initial buffer. Once you have that, build toward 1–3 months of essential expenses. Use a separate savings account with easy access but not linked to your checking card to reduce temptation.

4. Use the 50/30/20 framework (modified)

The classic 50/30/20 can be tweaked for low-income earners:

- Needs: 60–70% (housing, utilities, groceries, transportation)

- Wants: 5–10% (small discretionary spending)

- Savings/Debt repayment: 20–30% (emergency fund, high-interest debt)

Adjust percentages based on local costs and priorities. The key is intentional allocation.

5. Automate what you can

Automate savings transfers—even $10/week—so you don’t rely on willpower. Automate bill payments to avoid fees and protect your credit. Small, automated actions add up without daily effort.

Practical Ways to Save Money Every Day (Frugal Living)

Frugal food strategies

- Meal plan weekly and make a grocery list—stick to it.

- Buy generic brands and bulk staples (rice, beans, pasta, oats).

- Cook in batches and freeze portions to save time and reduce waste.

- Use apps and store loyalty cards for discounts; check local food banks if needed.

Lower housing and utility costs

- Consider roommate options or downsizing if feasible.

- Negotiate rent or ask about lease incentives; document polite, respectful negotiation tactics.

- Reduce energy use: LED bulbs, smart power strips, thermostat adjustments.

- Seek utility assistance programs and community resources for heating or water bills.

Transportation savings

- Use public transit, bike, walk, or carpool to cut fuel and maintenance costs.

- Schedule preventative maintenance to avoid expensive repairs.

- Shop around for car insurance—ask for discounts and safe-driver programs.

Smart shopping & avoiding impulse buys

- Wait 24–48 hours before non-essential purchases to prevent impulse buys.

- Buy secondhand clothes and furniture from thrift stores or online marketplaces.

- Use price comparison tools and browser extensions that apply coupon codes automatically.

Cut subscription costs

List monthly subscriptions and streaming services. Cancel or pause what you rarely use. Share family plans where allowed to lower per-person costs.

Low Salary Strategies: Increase Income Without a Full Career Change

Side hustles that fit a tight schedule

- Freelancing: writing, graphic design, data entry (Upwork, Fiverr).

- Gig economy: food delivery, rideshare, grocery shopping (when net returns are positive).

- Microtasks & surveys: small payouts but flexible.

- Sell unused items online—declutter and earn cash.

Boost skills affordably

Many free or low-cost courses exist (Coursera, Khan Academy, community college classes). Target high-return skills for side income: basic coding, bookkeeping, digital marketing, or trades.

Ask for raises intelligently

Prepare a case: document accomplishments, market rates, and positive performance reviews. Practice a respectful script and timing—after a strong project or during performance reviews.

Use benefits and credits

File taxes to claim credits (Earned Income Tax Credit, Child Tax Credit where eligible). Use employer benefits—401(k) matching, flexible spending accounts, commuter benefits—to stretch your paycheck.

Managing Debt: Smart Repayment Methods

Snowball vs. avalanche—choose what motivates you

Snowball: pay smallest balances first to gain momentum. Avalanche: pay highest-interest debt first to save money long-term. Both work; pick the one you’ll stick with.

Negotiate and consolidate

Contact creditors to ask for hardship plans, lower interest rates, or extended payment plans. Consolidation loans or balance-transfer credit cards can lower rates—but watch for fees and promotional expirations.

Avoid predatory lending

Steer clear of payday loans and high-fee short-term credit. Use community credit unions or nonprofit credit counseling if you need help creating a sustainable plan.

Safety Nets & Public Resources to Leverage

Government and nonprofit programs

- SNAP (Supplemental Nutrition Assistance Program) for food support.

- LIHEAP (Low-Income Home Energy Assistance Program) for heating and cooling help.

- Local rent assistance, unemployment benefits, and community clinics for healthcare.

- 211 helpline or local social services for resource navigation.

Community resources

Food pantries, free tax-preparation assistance (VITA), workforce development centers, and libraries (free internet and courses) are valuable supports. Using these resources isn’t charity—it’s practical budgeting.

Frugal Habits That Protect Mental Health and Motivation

Financial stress affects well-being. Frugal living doesn’t mean deprivation—small comforts, social connections, and self-care are essential to staying motivated.

- Keep a modest “fun fund” for occasional treats that recharge you.

- Celebrate micro-wins (first $100 saved, a paid-off bill) to build momentum.

- Use free community events, parks, and library programs for low-cost social life.

Real-World Example: How Small Changes Add Up

Scenario: Income $1,800/month after taxes. Current state: No savings, $200 in monthly miscellaneous spending, $50 in subscriptions, $400 rent, $150 groceries, $150 transportation, $200 utilities & phone, $200 debt minimum payments.

Practical adjustments

- Track expenses for 30 days and identify $100 in avoidable spending (eating out, impulse buys).

- Negotiate phone bill and switch to a $40/month plan saving $60/month.

- Meal plan and bulk buy to reduce groceries by $40/month.

- Start an automated $50/month transfer to a separate emergency savings account.

Result: Within three months, emergency savings = $150 + $50 automated transfers = $150 (plus initial buffer). Monthly freed cash = $200, which is redirected to speed debt repayment. Over a year, $50/month saved = $600; $200/month extra toward debt accelerates payoff and reduces interest—tangible progress that builds confidence.

Tools, Apps, and Resources

Use tools that simplify budgeting and identify savings:

- Budgeting apps: Mint, EveryDollar, YNAB (You Need A Budget) — choose based on whether you want automation or hands-on control.

- Coupon & deal apps: Honey, Rakuten, local grocery apps for digital coupons.

- Local resources: 211.org to find community assistance; IRS VITA for free tax filing if eligible.

Internal link suggestion: Link to a related article on “How to Build an Emergency Fund on a Low Income” using anchor text “build an emergency fund.”

External link suggestions: Link to official resources such as usa.gov benefits (https://www.usa.gov/benefits) and the Consumer Financial Protection Bureau (https://www.consumerfinance.gov/) when discussing protections and programs.

Frequently Asked Questions (FAQ)

Q: How can I start saving if I barely cover my bills?

A: Start extremely small—$5 or $10 a week. Focus on cutting one recurring expense, meal planning to lower grocery bills, and exploring assistance programs. Momentum matters more than instant perfection.

Q: Is it better to pay off debt or save first?

A: Build a small emergency fund ($500–1,000) first to avoid new debt, then tackle high-interest debt while keeping a steady savings habit. Adjust based on interest rates and risk tolerance.

Q: What’s the best budgeting method for someone with irregular income?

A: Use a “baseline budget” based on your lowest recent monthly income. Prioritize essentials, save extra income when it appears, and use a separate account for irregular expenses.

Quick Start Checklist: Take Action This Week

- Track every expense for 7 days—note even small cash purchases.

- Create a simple zero-based budget for next month and automate a small transfer to savings.

- List monthly subscriptions and cancel at least one you rarely use.

- Meal plan for the next week and shop from a list to cut food waste and costs.

- Contact one creditor to inquire about a hardship plan or lower interest options.

Conclusion

Thriving on a budget is less about deprivation and more about intentional choices. With clear budgeting tips, frugal living techniques, and low salary strategies, you can reduce financial stress, make steady progress toward savings, and create opportunities for better days ahead. Start small, automate what you can, and use community resources when needed. Each incremental action compounds into stability—so begin today and celebrate every win along the way.

Take the first step: Track your expenses for one week and set up an automated transfer of just $10 to a separate savings account. That tiny habit is the beginning of real change.

SEO & Publication Details

Primary keywords used: budgeting tips, saving money, low salary strategies, frugal living (integrated naturally). Suggested meta description is included in the page head. Recommended H1/H2/H3 structure is implemented. Suggested internal link anchor: “build an emergency fund.” Suggested external authoritative links: USA.gov benefits, Consumer Financial Protection Bureau, IRS VITA. Recommended image ideas with alt text:

- Image 1: Person writing a budget in a notebook. Alt text: “Person creating a monthly budget—budgeting tips for low-income earners.”

- Image 2: Simple meal prep containers on a table. Alt text: “Frugal living meal prep to save money on groceries.”

- Image 3: Hands placing coins into a jar labeled ‘Emergency Fund’. Alt text: “Saving money and building an emergency fund on a low salary.”

Schema recommendation: Use Article schema with author, datePublished, headline, description, mainEntityOfPage, and suggested keywords. Ensure external links open in a new window (target=”_blank”) and internal links open in the same window.

Social sharing optimization: Add share buttons with prefilled text—e.g., “Thriving on a Budget: Practical tips for saving money on a low salary” and include the URL and relevant hashtags (#FrugalLiving #BudgetingTips #SavingMoney).